Overview: The dog days of August for the Northern Hemisphere are here and the capital markets are relatively subdued. Equities are firmer. The notable exceptions in Asia was China, Hong Kong, and Taiwan. The MSCI Asia Pacific Index has advanced for the last three weeks. Europe’s Stoxx 600 slipped almost 0.6% last week and has recouped most of it today. US futures are steady to firmer. The US 10-year yield is struggling to stay above 2.8%, while European benchmarks are off 3-6 bp, with Italian yields firmer after Moody’s cut the country’s credit outlook to negative before the weekend. The dollar is mostly softer with the Australian and New Zealand dollar’s leading the way (~0.60%-0.75% better). The euro and yen are little changed. Among emerging market currencies, the Asian Pacific complex is softer while the central European currencies, South African rand, and Mexican peso enjoy a firmer tone. Gold is trading quietly in a $4-range centered near $1775. September WTI was sold back down after it tried to resurface above $90 a barrel. OPEC and IEA provide new market assessments tomorrow. US natgas is heavier for the third consecutive session, while Europe’s benchmark is up 2%, is first gain in five sessions. Iron ore snapped a five-day fall ahead of the weekend with a 3.2% advance. It is up another 2.25% today. September copper rose in the last two sessions, but it is struggling today. September wheat fell almost 4% last week and is off nearly another 1% today. At the end of the week, the US Department of Agriculture updates its World Agriculture Supply and Demand Estimate.

Asia Pacific

China's July trade surplus

rose to a new record of $101 bln after $97.9 bln in June. Exports edged up slightly, rising 18%

year-over-year after a 17.9% increase previously. Economists had expected

exports to slow to around 14%. Imports rose 2.3%, a little more than half what

was projected, but more than double June's 1% increase. While imports of crude

oil increased, only commodities, such as soy, copper, natural gas. The sluggish

growth in imports is thought to reflect soft domestic demand. However, the

economy does appear to be recovering from the contraction earlier this year.

Japan, on the other hand,

has seen a deterioration of the terms of trade and recorded a JPY1.37 trillion

trade deficit in June, which drove the current account into a deficit of

JPY132.4 bln, the first since January. To put the trade deficit in balance-of-payment terms in a

context, consider that it ran a surplus of about JPY2.28 trillion in H1 21 and

a JPY5.66 trillion deficit in H1 22. Separately, we note that the speculative

positioning in the futures market showed a roughly 18k contract reduction of

the net short yen position in the week ending August 2. At about 42.7k

contracts (each worth ~$95k), it is the smallest net short position since June

2021. Lastly, and arguably with the least direct economic implications, press

reports have confirmed what has swirled around for several days, namely a

cabinet reshuffle that Prime Minister Kishida is expected to announce Wednesday.

The powerful ministries of finance, industry, and foreign affairs are not

expected to change. Given that there ae no national elections for three years,

Kishida may be re-balancing the three main factions in the LDP now: his,

Abe, and Aso (LDP Vice President). It looks like the Abe faction may be weaker

for obvious reasons. The latest polls show public support for the cabinet is

waning but still above 55%. Still, changing a few top ministers is unlikely to

hurt and maybe even help.

Foreign investors sold

around $430 mln of Taiwanese equities last week which brings the

quarter-to-date liquidation to $1.06 bln. In H1, foreign investors sold almost $34

bln of Taiwanese shares. News that officials would support the equity and

currency markets helped stabilize the Taiex and the Taiwanese dollar. The Taiex

recouped the week's losses plus a little more with a 2.25% surge at the end of

last week. Similarly, the Taiwanese dollar rose by almost 0.15% ahead of the

weekend, allowing it to close with a miniscule advance for the week. While

Taiwan's reserves are little changed this year, Hong Kong Monetary Authority's

defense of the peg has been persistent. Its reserves, while still plentiful at

nearly $442 bln, have fallen by more than $55 bln over the past eight months. This

means HK may account for almost half of the $116 bln decline in the Federal

Reserve's custody holdings of Treasuries and Agencies for foreign central banks

over this period. South Korea's reserves have fallen steadily since the end of

last year and are now around $30 bln lower. Thailand's reserves have fallen by

$26 bln this year after $12 bln last year. The Philippine's reserves have

fallen for the past five months and six of the past seven for a cumulative loss

of about $10 bln. Lastly, China's July reserves rose $32.8 bln to $3.10

trillion from $3.07 trillion. It was only the second increase in reserves this

year and appears to be largely the result of valuation adjustments: the

dollar and yields fell. Year-to-date, China's reserves have fallen by around

$146 bln.

The US dollar edged slightly

above the job-induced high against the Japanese yen seen ahead of the weekend,

stalling near JPY135.60. It

peaked on July 14 around JPY139.40 and fell to JPY130.40 last week. The

recovery in US yields has helped the greenback recoup more than half of the

decline. The JPY136 area corresponds to the (61.8%) retracement objective. Initial

support is around JPY134.80. The Australian dollar has nearly recovered its

pre-weekend losses to test the $0.6975 area. A band of resistance

extends to $0.7000 and last week's high was closer to $0.7050. We look for a

heavier Aussie in the North American session, with potential toward the

$0.6900-20 area. Meanwhile, the greenback is slightly firmer against the

Chinese yuan above CNY6.76. Yet, it is within the new range that has developed

in recent weeks between roughly CNY6.7280 and CNY6.7820. The PBOC set the

dollar's reference rate tightly against expectations (CNY6.7695 vs. CNY6.7693).

Europe

Before the weekend, Moody's

cut the outlook for Italy's rating to negative from stable. It cited the accumulation of risks

stemming from Russia's invasion of Ukraine and the political uncertainty

following the collapse of the Draghi government. Of the three large rating

agencies, Moody's is the toughest on Italy. It assigns a Baa3 rating to it,

which is one notch above junk and one notch below S&P and Fitch. Late last

month, S&P revised its rating outlook for Italy to stable from positive. Fitch

has had a stable outlook. Last week, Italy's premium over Germany on 10-year

rates fell 14 bp, including nearly half (six basis points) ahead of the weekend

to near 2.06%, a three-week low. It has given the pre-weekend gains back

and is near 2.13%. At the two-year tenor, Italy's premium fell 30 bp to 0.81%,

the least since mid-July and has also recovered the pre-weekend decline and is

near 0.89%.

With a national election

next month Italy's political drama is center stage. Meloni, the head of the Brothers of Italy,

who could become the next prime minister (and first woman) is not from the part

of the Italian right that is anti-EU, anti-NATO. To the contrary, she committed

to the reforms that will unlock more of the EU's Next Generation funds, for

which Italy could be the largest beneficiary. The center-left looks like its

flailing. A coalition announced on Saturday was abandoned on Sunday. Without a

credible coalition the polls warn that the center-right can win as much as

three-quarters of both chambers of parliament. Meanwhile, the flexibility

the ECB has secured in reinvesting the maturing proceeds from the Pandemic

Emergency Purchase Program already appears to have been utilized to support the

peripheral bond markets.

In addition, to the

disruptions spurred by Russian's invasion of Ukraine, post-Covid supply chain

disruptions, and the tightening of monetary policy, the extreme weather in

Europe is also exacerbating economic tensions. It is the driest in Britain in

90-years according to some estimates. The Rhine River is becoming too shallow

for transport of heavy materials, and French nuclear plants have been given a

temporary waiver to dump hot water in the rivers that are meant to help cool

the plants.

The euro is in a little more

than a half-of-a-cent range today below $1.0215. The pre-weekend low, after the US jobs

report was slightly above $1.0140. Today's low, set in Asia, was near $1.0160. The

single currency does not appear to be moving quickly anywhere and appears

comfortable in a $1.01-$1.03 range. That said, we do not have much confidence

in its resilience in the face of the widening of the US 2-year premium over

Germany. It stands at a new high today of 2.80%, the most since May 2019. Sterling

is trading quietly in a $1.2050-$1.2125 range today, easily inside the

pre-weekend range (~$1.2000-$1.2170). The economic highlight of the week

comes Friday with the preliminary look at Q2 GDP. A small contraction is

expected. Despite downside risks, the Bank of England is expected to deliver

another 50 bp hike next month (~88% chance discounted in the swaps

market).

America

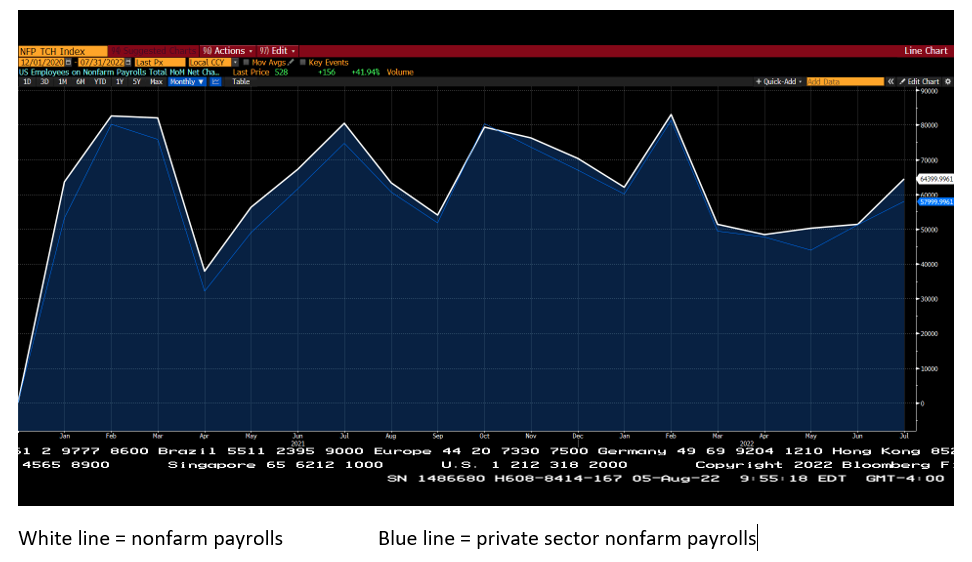

The softness seen in the

weekly jobless claims and ISM surveys was countered by the strong employment

report. Almost 530k jobs

positions were filled last month, more than twice expectations. The

establishment survey has now fully made up for the losses during the pandemic,

though if the public health crisis did not take place, the total number of

employment could be around 2.0.2-5 mln higher. It also suggests that much of

focus on the number of layoffs announced last month was sensationalist. It is

not that it is fake news, but distorted news especially when portrayed as

reflective of broad developments.

Fed Chair Powell says price

pressures are straightforward enough that one number, headline PCE captures it.

However, the labor market

is more complex, he says. Several other elements of the employment report

reflected a still-robust labor market, including the 0.4% increase in aggregate

hours (good sign for GDP), and a 0.5% rise in hourly earnings (and an upward

revision in the June series to 0.4% from 0.3%). The unemployment rate slipped

to a new low of 3.5%, though it partly is a function of the fall in the

participation rate to 62.1% from 62.2%. The teenage participation rate seemed

to have been a factor. Where does this leave the US economy at the start of

Q3? The PMI and Fed surveys data disappointed, but the ISM survey was

better, and two real sector reports, auto sales and jobs saw some momentum not

seen at the end of Q2.

Without fresh

"leaks", the market realizes that the strength of the jobs report

eases the pressure to recognize the current situation as a recession and boosts

the chances of a 75 bp rate hike next month. Some apparently have suggested the risk of an inter-meeting

move, but the market is not really biting. Fair value for the August Fed funds

futures, assuming no inter-meeting hike, is 97.67 (2.33%), and the contract

closed at 97.655 (2.345%). The futures strip shows the year-end rate to be

3.56%, a 25 bp increase on the week. Recall the July high was 3.68% and the

June high was 3.72%.

US consumer credit soared by $40.2 bln in June, half again as much as expected. It is the second-highest on record. Consumer credit has accelerated this year. It rose $100 bon in Q1 and another $100 bln in Q2. In all of last year, consumer credit rose by almost $250 bln. Notably, revolving credit (credit cards) rose by $14.8 bln in June, slightly above the recent average. Non-revolving debt grew by $25.4 bln. As this chart of consumer credit shows, it typically falls sharply in a recession.

The divergence of the jobs' reports before the weekend, weighed on

the Canadian dollar, even though the S&P 500 recouped most of its early

losses. Canada shed full-time jobs for the second consecutive month and

saw decline in the participation rate. The US dollar reached CAD1.2985,

its highest level in two-and-a-half weeks. It is consolidating today in a

30-pip range on either side of CAD1.2920. The re-assessment of the

trajectory of Fed policy plus the drop in oil prices comes as the momentum

indicators turn up for the greenback. We suspect the path of least

resistance is higher for the greenback. Initially, we look for CAD1.3050,

and maybe CAD1.31. Mexico reports CPI figures tomorrow. Price pressures are still accelerating, and this will likely

lead to another 75 bp rate hike (same as in June), which would lift the

overnight target to 8.5%. The swaps market sees another 100 bp after this

week's hike over the next six months. The US dollar peaked last week near

MXN20.83 and finished the week around MXN20.4050. It tested the

MXN20.3060 area today. Support is seen in the MXN20.20-MXN20.23

band. A break could target the MXN20.00-05 area, we would be more

inclined to fade it. Note that Brazil reports its IPCA inflation measure tomorrow,

and it is expected to fall to its lowest level of the year, slightly above 10%.

It peaked in April at 12.1%. The dollar fell almost 1% against the

Brazilian real before the weekend. Last week's low was set near

BRL5.13. A break of the BRL5.10 area could spur a test on BRL5.0.

Disclaimer

Reviewed by Marc Chandler

on

August 08, 2022

Rating:

Reviewed by Marc Chandler

on

August 08, 2022

Rating: