After disparaging the French Revolution at

the Paris G7 summit in 1989, Margaret Thatcher left a copy of Dicken's Tale of

Two Cities for the French Socialist President Mitterand. The story, as it will be recalled, contrasts the revolutionary chaos

of Paris in 1789 to the peaceful London. The French Revolution was also

the subject of the seeming misunderstanding of Chinese premier Zhou Enlai who,

when asked in 1972 about the political implication, said it was too soon to

tell. The apocryphal account is now widely recognized as a

misunderstanding and that Zhou's comment referred to the French student

protests of 1968.

In any event, the opening sentence of the book captures the spirit of the capital markets as Q3 is winding is down. The second quarter was horrific; it appears for nearly everyone but China. Economies bounced back sharply in Q3, and the issue that the high-frequency data will shed light on is just how strong of a recovery. The MSCI free-float weighted world equity index (includes developed and emerging markets) made a new record high in early September before the current correction.

Economic reports from most of the major economies show the pace of the recovery has slowed. In the same way, the recovery began before the end of the Q2, the loss of economic momentum was seen as early as July in some series and August in others. The deceleration is catching economists by surprise. That was the take away from the August US industrial production and retail sales reports last week. Industrial output rose by 0.4%, which was less than half of the median forecast (Bloomberg survey). Retail sales rose 0.6% in August, not the 1% economists forecast, and, to add insult to injury, July's shopping spree was revised to 0.9% from 1.2%.

The main economic report for the major industrial countries next week is the preliminary PMI surveys for September. The US and UK composite made new highs in August, but Japan has gone now where since recovering to 45.0 in June, and the eurozone peaked in July and slipped in August. And the sentiment indicators seem to be running ahead of the hard data.

At the same time, price pressures in most countries remained too low for policymakers' comfort. Oil prices are off a third despite the dramatic recovery from April when negative prices in the futures market were seen. The disruption spurred by the pandemic and the policy response as distorted prices and shifting consumption patterns. Cuts in the sales tax (value-added tax, e.g., Germany), different seasonal promotional sales schedules, and lower housing costs (rents and owner-occupied costs) weigh on core measures. Just like some scoff at annualized quarterly GDP figures, projecting the low inflation figures far into the future also does not seem right.

The role of the euro in the region's inflation has become a talking point in recent weeks. The argument is that the euro's rise will dampen EMU inflation. It seems reasonable but there are two considerations that caution against exaggerating. First, the euro's rise against the dollar is modest. It is not fair to measure it from its extremes. The euro was flat in the first half of the year. It rallied in July by the most in a decade, but since the end of July, with some exceptions around the Fed's announcement of an average inflation target, the euro has been mostly chopping sideways between $1.17 and $1.19.

Second, many other factors influence eurozone inflation than the bilateral exchange rate, which the ECB says in monitors but does not target. Consider that in 2015 and 2016, when the euro average (ave monthly close) was around $1.1030, headline CPI was 0.2% (12-month average). In 2017, the euro average almost $1.14, and CPI averaged 1.5%. In 2018, the euro a little below $1.1780, while the CPI averaged 1.8%. Last year the euro averaged almost $1.12. CPI averaged 1.2%. For the sake of the argument, imagine the euro averages $1.20 in the last four months of 2020, then the average this year would be a little above $1.15. Through August, EMU CPI has averaged 0.5%.

Of course, there are variable and unpredictable lags and leads, but monetary union means that Europe has transformed from a group of mostly small open economies to a large, less open economy. Surely, the 35% decline in oil prices, year-to-date, has deflationary implications, including core services, like transportation. There is still more than six months before the March and April oil shock drops from year-over-year measures.

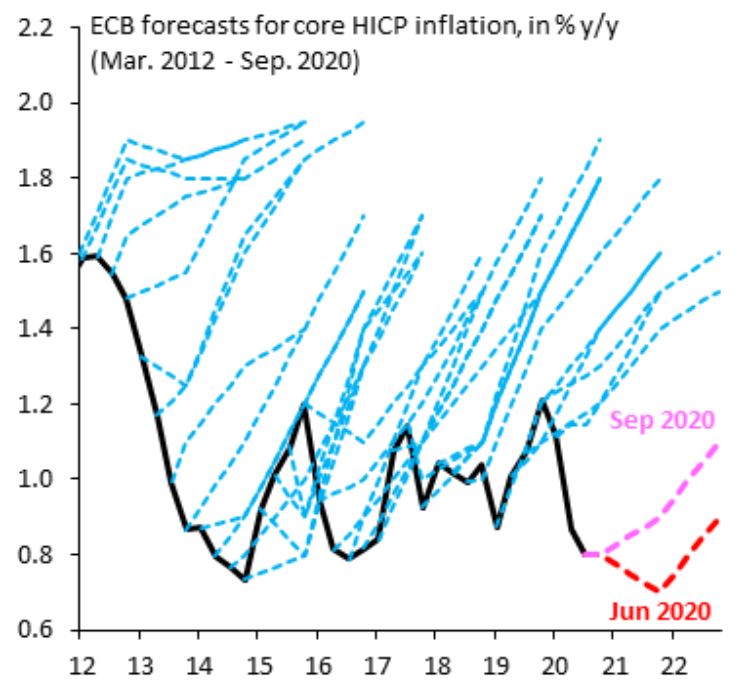

It seems perfectly reasonable for the exchange rate to be an input into models that measure financial conditions and estimate inflation. However, the ECB's ability to forecast inflation is rather weak, as this chart from the Institute of International Finance illustrates. This is most certainly not meant to throw shade at the ECB's economic staff. Instead, it is about the ability to forecast inflation in general. The chart shows that over the period in which the euro has been weak (it has been below the OECD's measure of purchasing power parity since mid-2014), the ECB has consistently anticipated greater inflation than materialized, even if adjusted for lags.

It seems perfectly reasonable for the exchange rate to be an input into models that measure financial conditions and estimate inflation. However, the ECB's ability to forecast inflation is rather weak, as this chart from the Institute of International Finance illustrates. This is most certainly not meant to throw shade at the ECB's economic staff. Instead, it is about the ability to forecast inflation in general. The chart shows that over the period in which the euro has been weak (it has been below the OECD's measure of purchasing power parity since mid-2014), the ECB has consistently anticipated greater inflation than materialized, even if adjusted for lags.

Inflation (and interest rates) have been trending lower for around 40 years. All the things that economists have said would cause inflation, like the dramatic expansion of central bank balance sheets, negative interest rates, extending promises of low-interest rates for longer, etc. etc., have lifted prices, and this was before the pandemic. It is difficult to imagine that more of the same, on top of the economic disruption of Covid is going to materially change the outcome. St. Louis Fed President Bullard explained that there are understandable relationships between macroeconomic variables in a specific paradigm and when the paradigm shifts the relationships change.

The major central banks have met in recent weeks, and all seemed to promise more actions if needed. Investors are concluding more support will be provided. A Covid vaccine is a wild card, especially if President Trump is right, and a vaccine will be available before the November election. However, assuming that other health officials are correct and a credible vaccine will take at least 6-9 months longer, more monetary support is likely.

Of the major central banks, the Bank of England may be the first to move and possibly at its next meeting in November. It is unlikely to be ready for negative interest rates, but zero-interest rates and/or more Gilt purchases seem reasonable. The ECB is expected to extend its Pandemic Emergency Purchase Program at the December meeting and extend it until the end of next year. The market appears to be pricing in a 10 bp rate cut, and partly as a result, three-month Euribor traded below the ECB's deposit rate (-0.5%) for the first time last week. The EU will continue to recognize fiscal flexibility in 2021, and budget deficits throughout the region are likely to remain elevated.

The Bank of Japan revised up its economic assessment at last week's meeting. Yet, Japan's core measure of inflation, which excludes fresh food but includes energy, fell to -0.4% year-over-year in August. Tourism promotion, including discounts, are estimated to shave CPI measures by 0.3%-0.4%. Similarly, in Europe, disinflation, for sure, deflation probably not. Japan's new prime minister enjoys a bump of popular support. If Suga seeks his own mandate by insisting on elections, he will also likely push for another supplemental budget. The BOJ may want to accommodate the new prime minister.

The Federal Reserve's average inflation regime is just dressed up forward guidance. The Fed's own projections indicate that it does not expect to reach its goals for at least three years. Simply because the Fed is "independent" does not mean that it is not a valid question whether that is acceptable. Who determined that a three-year wait is a reasonable price for not taking new measures. The US economy may be one poor jobs report from intensifying pressure on the Fed to act. One way or the other, the political paralysis in Washington that is preventing additional stimulus will change come November. A majority of both Republicans and Democrats favor additional support. It is a question of when and how much.

Economic reports from most of the major economies show the pace of the recovery has slowed. In the same way, the recovery began before the end of the Q2, the loss of economic momentum was seen as early as July in some series and August in others. The deceleration is catching economists by surprise. That was the take away from the August US industrial production and retail sales reports last week. Industrial output rose by 0.4%, which was less than half of the median forecast (Bloomberg survey). Retail sales rose 0.6% in August, not the 1% economists forecast, and, to add insult to injury, July's shopping spree was revised to 0.9% from 1.2%.

The main economic report for the major industrial countries next week is the preliminary PMI surveys for September. The US and UK composite made new highs in August, but Japan has gone now where since recovering to 45.0 in June, and the eurozone peaked in July and slipped in August. And the sentiment indicators seem to be running ahead of the hard data.

At the same time, price pressures in most countries remained too low for policymakers' comfort. Oil prices are off a third despite the dramatic recovery from April when negative prices in the futures market were seen. The disruption spurred by the pandemic and the policy response as distorted prices and shifting consumption patterns. Cuts in the sales tax (value-added tax, e.g., Germany), different seasonal promotional sales schedules, and lower housing costs (rents and owner-occupied costs) weigh on core measures. Just like some scoff at annualized quarterly GDP figures, projecting the low inflation figures far into the future also does not seem right.

The role of the euro in the region's inflation has become a talking point in recent weeks. The argument is that the euro's rise will dampen EMU inflation. It seems reasonable but there are two considerations that caution against exaggerating. First, the euro's rise against the dollar is modest. It is not fair to measure it from its extremes. The euro was flat in the first half of the year. It rallied in July by the most in a decade, but since the end of July, with some exceptions around the Fed's announcement of an average inflation target, the euro has been mostly chopping sideways between $1.17 and $1.19.

Second, many other factors influence eurozone inflation than the bilateral exchange rate, which the ECB says in monitors but does not target. Consider that in 2015 and 2016, when the euro average (ave monthly close) was around $1.1030, headline CPI was 0.2% (12-month average). In 2017, the euro average almost $1.14, and CPI averaged 1.5%. In 2018, the euro a little below $1.1780, while the CPI averaged 1.8%. Last year the euro averaged almost $1.12. CPI averaged 1.2%. For the sake of the argument, imagine the euro averages $1.20 in the last four months of 2020, then the average this year would be a little above $1.15. Through August, EMU CPI has averaged 0.5%.

Of course, there are variable and unpredictable lags and leads, but monetary union means that Europe has transformed from a group of mostly small open economies to a large, less open economy. Surely, the 35% decline in oil prices, year-to-date, has deflationary implications, including core services, like transportation. There is still more than six months before the March and April oil shock drops from year-over-year measures.

It seems perfectly reasonable for the exchange rate to be an input into models that measure financial conditions and estimate inflation. However, the ECB's ability to forecast inflation is rather weak, as this chart from the Institute of International Finance illustrates. This is most certainly not meant to throw shade at the ECB's economic staff. Instead, it is about the ability to forecast inflation in general. The chart shows that over the period in which the euro has been weak (it has been below the OECD's measure of purchasing power parity since mid-2014), the ECB has consistently anticipated greater inflation than materialized, even if adjusted for lags.

It seems perfectly reasonable for the exchange rate to be an input into models that measure financial conditions and estimate inflation. However, the ECB's ability to forecast inflation is rather weak, as this chart from the Institute of International Finance illustrates. This is most certainly not meant to throw shade at the ECB's economic staff. Instead, it is about the ability to forecast inflation in general. The chart shows that over the period in which the euro has been weak (it has been below the OECD's measure of purchasing power parity since mid-2014), the ECB has consistently anticipated greater inflation than materialized, even if adjusted for lags.Inflation (and interest rates) have been trending lower for around 40 years. All the things that economists have said would cause inflation, like the dramatic expansion of central bank balance sheets, negative interest rates, extending promises of low-interest rates for longer, etc. etc., have lifted prices, and this was before the pandemic. It is difficult to imagine that more of the same, on top of the economic disruption of Covid is going to materially change the outcome. St. Louis Fed President Bullard explained that there are understandable relationships between macroeconomic variables in a specific paradigm and when the paradigm shifts the relationships change.

The major central banks have met in recent weeks, and all seemed to promise more actions if needed. Investors are concluding more support will be provided. A Covid vaccine is a wild card, especially if President Trump is right, and a vaccine will be available before the November election. However, assuming that other health officials are correct and a credible vaccine will take at least 6-9 months longer, more monetary support is likely.

Of the major central banks, the Bank of England may be the first to move and possibly at its next meeting in November. It is unlikely to be ready for negative interest rates, but zero-interest rates and/or more Gilt purchases seem reasonable. The ECB is expected to extend its Pandemic Emergency Purchase Program at the December meeting and extend it until the end of next year. The market appears to be pricing in a 10 bp rate cut, and partly as a result, three-month Euribor traded below the ECB's deposit rate (-0.5%) for the first time last week. The EU will continue to recognize fiscal flexibility in 2021, and budget deficits throughout the region are likely to remain elevated.

The Bank of Japan revised up its economic assessment at last week's meeting. Yet, Japan's core measure of inflation, which excludes fresh food but includes energy, fell to -0.4% year-over-year in August. Tourism promotion, including discounts, are estimated to shave CPI measures by 0.3%-0.4%. Similarly, in Europe, disinflation, for sure, deflation probably not. Japan's new prime minister enjoys a bump of popular support. If Suga seeks his own mandate by insisting on elections, he will also likely push for another supplemental budget. The BOJ may want to accommodate the new prime minister.

The Federal Reserve's average inflation regime is just dressed up forward guidance. The Fed's own projections indicate that it does not expect to reach its goals for at least three years. Simply because the Fed is "independent" does not mean that it is not a valid question whether that is acceptable. Who determined that a three-year wait is a reasonable price for not taking new measures. The US economy may be one poor jobs report from intensifying pressure on the Fed to act. One way or the other, the political paralysis in Washington that is preventing additional stimulus will change come November. A majority of both Republicans and Democrats favor additional support. It is a question of when and how much.

Disclaimer

It was the Best of Times, It was the Worst of Times

Reviewed by Marc Chandler

on

September 19, 2020

Rating:

Reviewed by Marc Chandler

on

September 19, 2020

Rating:

Reviewed by Marc Chandler

on

September 19, 2020

Rating: